What happens if a builder disappears after a deposit?

If a builder stops responding after a deposit, move quickly: collect evidence, stop further payments, contact your bank if fraud is suspected, and get consumer advice.

Slate

Slate guide

3 min read

If a builder disappears after taking a deposit, the first priority is to stop the damage getting worse. Do not send more money to restart communication. Do not rely on phone calls alone. Move everything into written records.

This guide is practical information, not legal advice. If the amount is significant or there are safety issues, get professional advice.

Collect the evidence

Create one folder with:

- the quote or contract

- invoices and receipts

- bank transfer records

- messages and emails

- photos of any work done

- agreed start dates

- the builder's business name and address

If you need help later, evidence will matter more than memory.

Decide whether it looks like a dispute or a scam

There is an important difference between a real trader dispute and a scam. If you think you have been tricked into sending money to a fraudster, contact your bank immediately.

If the payment was to a genuine trader and the disagreement is about performance, timing, or refund rights, your bank may treat it as a civil dispute. The Payment Systems Regulator has guidance on how payment firms distinguish APP scam claims from civil disputes: PSR APP scam and civil dispute guidance.

Send a clear written message

If it is safe to do so, send one concise written message. Include:

- the job reference

- the amount paid

- the agreed start date or work

- what has not happened

- what you want next

- a reasonable deadline for response

Avoid emotional back-and-forth. You are creating a record.

Get consumer advice

GOV.UK directs consumers with building work, poor service, contracts, rogue traders, and fraud issues to consumer advice services: Consumer rights.

Citizens Advice can explain next steps and may pass relevant information to Trading Standards.

Prevent the same risk next time

The hardest lesson is that recovery can be slower and less certain than prevention. Next time, avoid paying a large deposit without:

- a written quote

- a named payment stage

- verified bank details

- a record of what the deposit covers

- a clear refund or delay term

For prevention, read what is a reasonable builder deposit?.

FAQ

Can my bank reverse a builder deposit?

Possibly, but do not assume it can. Contact your bank quickly if fraud is suspected. If it is a civil dispute with a genuine trader, recovery may be different.

Should I keep calling the builder?

You can try, but make sure important requests are in writing. Written records are easier to rely on later.

Should I pay more if the builder says they need it to continue?

Be very cautious. Do not send more money until the existing issue is explained and a clear written plan is agreed.

Related guides

Keep reducing payment uncertainty

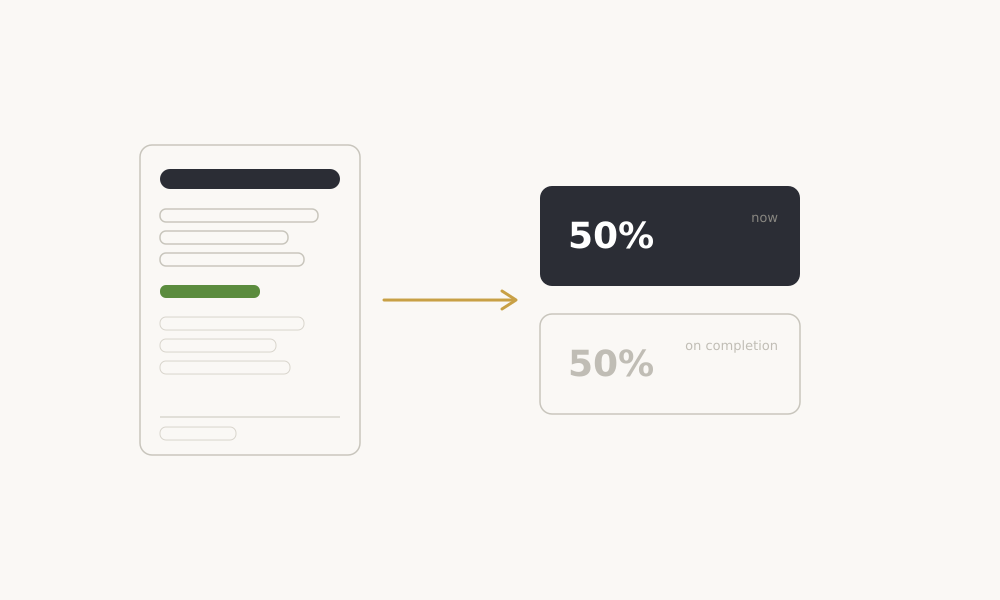

Is 50% upfront normal for builders?

A 50% builder deposit can be a warning sign unless it is tied to real materials, dates, and written milestones. Here is how to judge the risk before paying.

Questions to ask before paying a builder

Use these questions before paying a builder deposit, progress payment, or final invoice so the terms are clear before money moves.

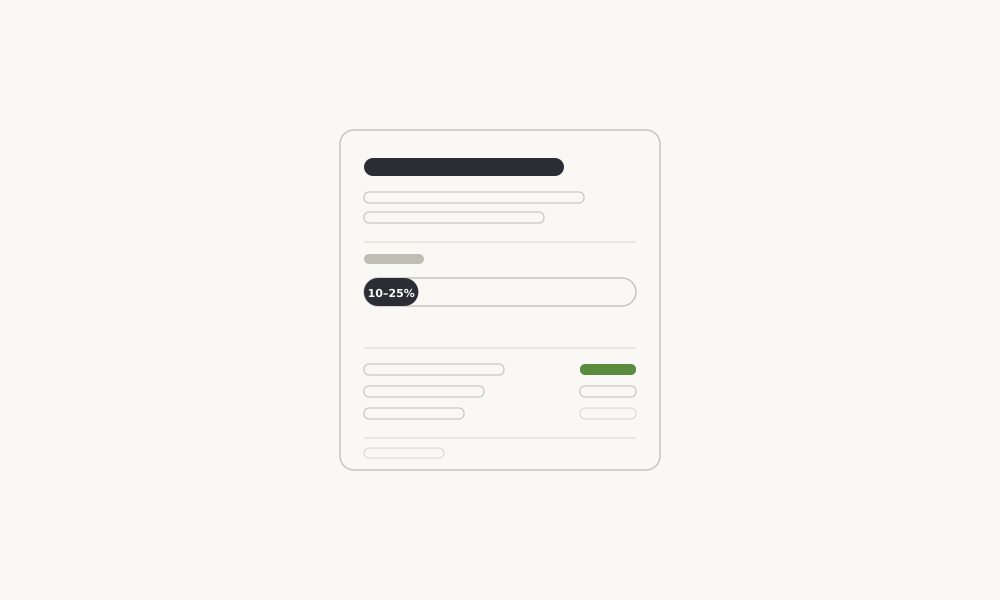

What is a reasonable builder deposit?

A reasonable builder deposit should match real upfront costs, not replace a payment schedule. Here is how to judge the amount before you pay.

How to avoid rogue traders

Rogue traders often rely on pressure, vague terms, and upfront payments. These checks help UK homeowners reduce risk before hiring.