Should you pay tradesmen by bank transfer?

Bank transfers are common for tradespeople, but they can be hard to reverse. Learn when they are sensible, when they are risky, and what checks to make first.

Slate

Slate guide

3 min read

Paying a tradesperson by bank transfer is common in the UK. It is fast, direct, and avoids card fees. But it also puts responsibility on you to make sure the recipient, invoice, and payment terms are right before you send the money.

The emotional risk is obvious: a bank transfer can feel final. If the work is not done, the payment is disputed, or the trader disappears, you may not have the same practical leverage you had before paying.

Bank transfer is not automatically unsafe

Many legitimate tradespeople prefer bank transfer. It gives them a clear payment record and can be easier to reconcile than cash.

The safer version looks like this:

- the payment goes to a named business account

- you have a written quote or invoice

- the invoice describes the work and payment stage

- the reference identifies the job

- the amount matches an agreed payment schedule

If any of those are missing, the transfer becomes harder to defend later.

The main risk with bank transfer

The main issue is that bank transfer payments are not designed like escrow or milestone payment systems. Once you authorise the payment, the money moves.

New UK reimbursement rules for authorised push payment scams apply to some scam cases from 7 October 2024, but they are not a general guarantee for every building dispute. The Payment Systems Regulator notes that civil disputes can be outside the reimbursement policy, and UK Finance explains that APP fraud is about being tricked into sending money to a criminal: UK Finance APP fraud guidance.

That distinction matters. If you paid a real trader and then the job went wrong, your bank may treat that as a dispute rather than a scam.

Checks before you transfer

Before paying by bank transfer:

- Check the account name matches the trader or company.

- Confirm the bank details through a second channel if they were sent by email or message.

- Avoid paying a personal account when the quote is from a limited company.

- Use a payment reference that names the job and milestone.

- Keep the quote, invoice, messages, and proof of payment together.

If the trader pressures you to transfer immediately, asks for cash instead, or changes account details late in the process, pause and verify.

Safer payment structure

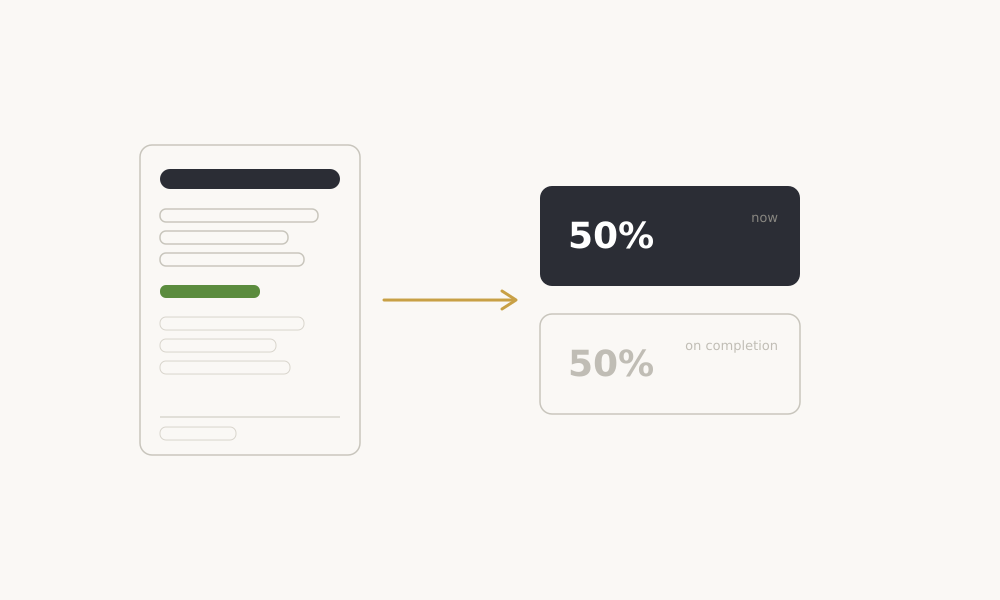

The payment method is only one part of the risk. The structure matters just as much.

Paying £500 by bank transfer after a clear milestone is less risky than paying £5,000 before work starts. A staged schedule gives both sides a record of what has been funded, completed, and approved.

For larger jobs, read how to safely pay contractors in the UK and payment schedules for home renovations.

FAQ

Is bank transfer safer than cash?

Usually yes, because it leaves a payment record. But a record does not guarantee you can recover the money if the work becomes a civil dispute.

Should I pay a deposit by bank transfer?

Only if the deposit is explained in writing and tied to a real cost or agreed stage. Avoid vague deposits that are only described as securing availability.

What if the bank details change?

Do not pay until you have verified the change through a trusted phone number or in-person conversation. Email account changes are a common fraud risk.

Related guides

Keep reducing payment uncertainty

Is 50% upfront normal for builders?

A 50% builder deposit can be a warning sign unless it is tied to real materials, dates, and written milestones. Here is how to judge the risk before paying.

How to safely pay contractors in the UK

A practical payment safety guide for UK homeowners hiring builders, decorators, landscapers, and other contractors.

How to avoid rogue traders

Rogue traders often rely on pressure, vague terms, and upfront payments. These checks help UK homeowners reduce risk before hiring.

What is a reasonable builder deposit?

A reasonable builder deposit should match real upfront costs, not replace a payment schedule. Here is how to judge the amount before you pay.